The only way to retire with financial security is by saving for retirement ASAP. Although setting aside retirement savings is a solid start in the right direction, making sure you’re saving enough toward your retirement goal is just as important.

Once you’ve decided how much you’ll contribute to your retirement fund, you’ll be closer to knowing if your savings are on track. Here’s how to get started.

The main takeaway is that you can get on track to retire at just about any age. But you have to be willing to commit to saving as much as you can and on a completely consistent basis.

Compound Earnings Catapults Your Retirement Fund

Building your retirement savings isn’t something you can do on a whim, work on for a few years, and then abandon. You need to set up a plan — and the earlier in life, the better — then commit to it for decades.

Why? Because compound earnings over time is what gets you to your retirement goal faster.

When you invest into your retirement, your funds earn interest. That interest is reinvested to earn more interest. This is the concept behind “compound interest”. To successfully plan for retirement, putting your contributions on auto-pilot is essential to maximize your compounded earnings.

This starts with opening the right to retirement plan, or even a combination of plans. From there, you can set up payroll deductions or automatic transfers from your bank account to fund whatever retirement plan you’ve chosen.

Choosing the Right Retirement Plan

You can start saving for retirement by participating in a workplace retirement plan, if your employer offers one. This will typically be a 401(k), 403(b), 457 or Thrift Savings Plan (TSP).

Under current tax contribution laws, you can contribute up to $19,500 per year to any of those plans, or $26,000 if you’re 50 or older. Some employers also offer a matching contribution that grows your savings fund more quickly.

A limitation of an employer-sponsored plan is that you’re often on your own to manage it. There might also be limited investment options, including some that have high investment fees. A good workaround for this problem is to sign up with a 401(k)-specific robo-advisor, like Blooom.

It’s a service that creates and manages a portfolio within your employer-sponsored plan, including replacing high-fee funds with those that charge lower fees. And it provides this service for a low, flat monthly fee. Your employer doesn’t need to be involved in the process — just add Blooom to your existing plan.

If You Don’t Have an Employer-Sponsored Retirement Plan

If you don’t have access to an employer-sponsored plan, you have a few options depending on your situation. Here are other types of retirement plans to consider:

Traditional IRA or Roth IRA. It can either include brokerage firms if you prefer self-directed investing, or robo-advisors if you’d rather have your investments managed for you. IRA contribution limits for either type of retirement plan let you contribute up to $6,000 per year, or $7,000 if you’re 50 or older. Here are a few places to open an IRA account.SEP-IRA. If you’re self-employed and a high-income earner, a SEP-IRA is the best way to build up a large retirement portfolio in less time. Rather than an annual contribution limit of $6,000 for traditional and Roth IRAs, the limit for a SEP-IRA is a whopping $57,000.Solo 401(k). A Solo 401(k) is also designed for self-employed workers (though it can also include a spouse who participates in the business). It has the same employee contribution limit as a standard 401(k) at $19,500 per year, or $26,000 if you are 50 or older. But a solo 401(k) lets you make an additional employer contribution to the plan up to $57,000 (or $63,500 if you are 59 or older). Employer contributions are also capped no more than 25{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} of your total compensation from your business. General Retirement Find Milestone Guidelines

The number of variables involved in retirement makes it impossible to come up with a specific savings goal to aim for in your situation. But like any plan, you’ll need to have milestones to let you know if you’re on track to retire or not.

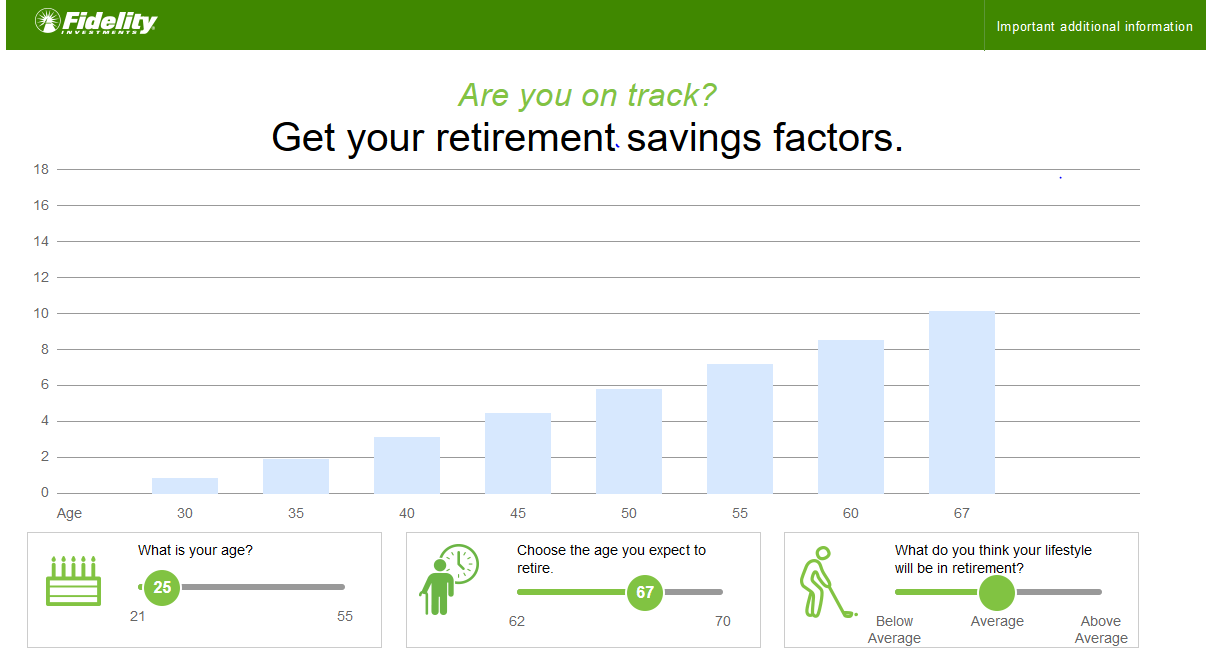

Although there are different methods of calculating retirement milestones, the Fidelity Retirement Widget offers the best ballpark figure. The widget is incredibly user-friendly, produces easy to understand results, and is absolutely free to use.

It determines how much money you should have at each age, based on your answers to three questions:

What is your current age?What age do you expect to retire?What do you think your lifestyle will be in retirement? (You can choose below average, average, and above average.)

The last question about your lifestyle in retirement is admittedly vague, but an educated guess is enough.

Plugging in a starting age of 25, with an expected age of retirement of 67, and an average lifestyle in retirement, Fidelity provided the following retirement milestones in five-year increments:

Each bar represents a multiple of your current annual income at a specific age. For example, at age 30, your total retirement savings should roughly equal your annual income. At 35, you should’ve saved double your income, and so on until age 67 when you retire.

At that point your retirement savings should be 10 times the amount of your annual income just before retiring. (It will be 12X your income at 67 if you expect an above average lifestyle, but just 8X if you expect to live a below-average lifestyle.)

How Accurate Are These Retirement Savings Milestones?

There’s no guaranteed method to project your exact future earnings or how much your retirement fund will compound over time. The best we can do is a ballpark estimate, especially if you’re only in your 20s or 30s.

But let’s work a loose example to demonstrate the validity of the Fidelity estimate.

Let’s say you reach 67, your final salary is $100,000, and you’ve accumulated 10 times that income in your combined retirement savings (i.e. $1 million).

It’s not reasonable to assume a $1 million portfolio will consistently generate 10{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} annual returns, fully replacing your $100,000 pre-retirement income.

General Rule of Thumb for Retirement Savings

Generally, you can plan on replacing 80{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} of your pre-retirement income. That means $80,000 per year of income in retirement. The reduction assumes you won’t have work-related expenses, like commuting, or making additional retirement contributions. It also assumes a lower annual tax bite. After all, once you retire, you’ll no longer be paying FICA taxes.

If you have a $1 million retirement portfolio, you can withdraw 4{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} per year without draining your portfolio to zero. This is what’s frequently referred to as the safe withdrawal rate.

Withdrawals of 4{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} will come to $40,000 on a $1 million portfolio. That will represent 50{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} of the $80,000 in needed retirement income.

Presumably, the rest will come from a combination of Social Security and any available pension income. You can use the Social Security Quick Calculator to determine what your benefits will be at retirement.

Using a Retirement Calculator to Track Your Goals

With your estimated Social Security benefits in mind, a retirement calculator can help you understand the remaining gap between your savings and how much you need for retirement.

For example, let’s say you’re 25-years-old, earning $50,000 annually, and your employer offers a 401(k) plan. For each of the remaining examples, we’ll assume your employer doesn’t match contributions, and assume a 7{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} annual rate of return on investments reflecting a mix of stocks and bonds in your plan.

If you want your 401(k) plan balance to match your salary by age 30, you’ll need to contribute

17{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} of your income — or about $8,500 per year — to your plan. With a 7{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} annual rate of return, that’ll give you a balance of $50,717.

If you expect to be earning $75,000 per year by the time you’re 35, you’ll need to have $150,000 in your plan by the time you reach that age.

Assuming your income averages $62,500 per year between the ages of 30 and 35, you’ll need to contribute 21{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} of your income, or $13,125 per year, to reach the $150,000 threshold in your plan.

The Magic of Saving for Retirement Early

Looking long-term, at retirement at age 67, let’s assume your income will grow to $100,000 between age 35 and 67. In this scenario, your average annual income is $87,500. Since you expect to earn $100,000 just before retiring, you should have $1 million sitting in your 401(k) plan.

What will it take to reach that goal?

Absolutely nothing!

One of the biggest and best secrets of retirement planning is the earlier in life you begin saving, the less you’ll need to save later on in life. And sometimes that’s nothing.

In this case, since you already have $150,000 in your plan at age 35, simply by investing the money at an average annual return of 7{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} for 32 years your plan will grow to $1.3 million. That’s without making even a single dollar of additional contribution.

And for what it’s worth, if you simply made the maximum 401(k) contribution of $19,500 each year between 35 and 67, your plan would have more than $3.4 million by the time you reach retirement.

The most fundamental rule of retirement savings planning is: save early and often!

Planning for Early Retirement

If you’re 25 years old and you want to retire at 50, decide how much income you’ll need to live on by the time you reach 50. Since you won’t have the benefit of Social Security or a pension, you’ll rely entirely on your retirement savings.

Let’s say you’ll need $40,000 per year to live in retirement. In this case, you’ll need to have $1 million in your retirement portfolio based on the 4{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} safe withdrawal rate.

How Much to Save for an Early Retirement

To get from $0 to $1 million in your retirement plan between 25 and 50, you’ll need to make the maximum 401(k) contribution allowed at $19,500 each year for 25 years. Assuming your investment produces a 7{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} return, you’ll have $1,181,209 by the time you reach 50. That’ll be a little bit higher than your $1 million retirement goal.

It’ll be difficult to carve out the full $19,500 on a $50,000 income you’re earning at age 25, but it gets easier as the years pass and your income increases. You might even decide to lower your contributions in your 20s, and work up to the maximum by the time you’re 30.

Just be aware that the foundational strategy of reaching early retirement is based on saving a seemingly ridiculous percentage of your income. Although others are saving 10{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} or maybe 15{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} of their income each year, you’ll need to think more in terms of 30{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31}, 40{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31}, or 50{e1706a52c3b3138427a8e72931d9d59b6d08ac610477d60aad46d317c02b8d31} savings. It all depends on how early you want to retire.

What to Do if You’re Not on Track to Retire

Unfortunately, this describes the majority of Americans. But it doesn’t need to be you, even if you’re not currently on track to retire.

Let’s say you’re 45 years old and earning $100,000, and you currently have $100,000 in total retirement savings. That means that at age 45 your retirement fund is where Fidelity recommends it should’ve been at age 30.

Don’t give up hope.

If you make the maximum contribution of $19,500 per year between ages 45 and 50, then increase it to the maximum of $26,000 per year from ages 50 to 65, you’ll have just over $1.3 million in your plan by the time you reach 65.

You won’t benefit from compound earnings that you would’ve seen had you started saving aggressively in your 20s, but your situation is far from hopeless.

The main takeaway is that you can get on track to retire at just about any age. But you have to be willing to commit to saving as much as you can and on a completely consistent basis.

The post Am I On Track to Retire? appeared first on Good Financial Cents®.

Read more: goodfinancialcents.com